Continued Investment in Purpose-built Rental Properties

This report provides a comprehensive analysis of the Build-to-Rent (BTR) investment landscape in Manchester and Stockport, UK, highlighting the robust fundamentals that underpin continued capital deployment in these key regional markets. The BTR sector nationally has demonstrated remarkable resilience and growth, driven by increasing institutional interest and a structural shift in the private rented sector. Manchester stands as a mature, high-growth BTR hub, characterized by strong economic and demographic drivers, a significant operational stock, and a substantial development pipeline. Conversely, Stockport is emerging as a dynamic, high-yield commuter town, benefiting from extensive urban regeneration and a compelling affordability proposition relative to its larger neighbour.

The analysis reveals that while both locations offer attractive investment prospects, their distinct market dynamics necessitate nuanced strategies. Manchester provides stability and scale for large-volume institutional capital, whereas Stockport presents opportunities for higher immediate rental growth and value appreciation through regeneration. Key challenges, including supply shortfalls, escalating costs, and evolving regulations, are identified, alongside strategies for mitigation. The report concludes with actionable recommendations for investors, emphasizing strategic asset allocation, engagement with regeneration initiatives, diversification of product types, and the imperative of integrating sustainability and placemaking into development strategies to ensure long-term viability and competitive advantage.

1. Introduction to the UK Build-to-Rent (BTR) Sector

Definition and Characteristics of BTR

The Build-to-Rent (BTR) sector encompasses residential properties specifically designed, constructed, and managed for long-term rental rather than individual sale. These developments are typically owned and operated by institutional investors or large-scale property management companies, distinguishing them from traditional buy-to-let investments. A core characteristic of the BTR model is its tenant-centric approach, which often includes a suite of communal amenities such as gyms, co-working spaces, resident lounges, and on-site management teams. This focus on providing a premium, professionally managed living experience, coupled with offerings of longer-term tenancies and predictable rents, has positioned BTR as an increasingly attractive option for both tenants and investors seeking to capitalize on the growing demand for high-quality rental accommodation.

National Investment Trends and Market Growth (2024-2025)

The UK BTR market has demonstrated exceptional momentum, achieving its fifth consecutive record year for investment in 2024, with total capital deployed surpassing £5 billion for the first time to reach £5.2 billion. This figure represents an 11% increase over 2023, underscoring sustained investor confidence in the sector. The final quarter of 2024 was particularly strong, accounting for £1.9 billion in transactions, with multifamily transactions comprising 71% of the investment value. This surge in multifamily deals also led to an increase in the average deal size, which reached £84 million in Q4, 3% above the long-term average.

In terms of supply, 2024 marked a record year for new delivery, with over 22,300 new BTR homes completed. This expanded the UK's operational BTR stock to over 126,000 homes, a 21% year-on-year increase. The pipeline remains robust, with a further 57,400 units currently under construction and 106,500 units having secured full planning permission, bringing the total size of the sector to 290,000 homes. The positive trend has continued into 2025, with the first quarter seeing over £800 million invested in UK BTR, including more than £500 million directed towards multifamily schemes in urban locations, indicating a renewed appetite for forward funding large-scale developments.

The consistent record investment in BTR, even amidst broader economic challenges, highlights the sector's perceived stability and attractiveness as an asset class. Factors such as high capital costs, rising construction expenses, regulatory uncertainties, and planning delays have impacted the wider UK housing sector. However, the sustained influx of capital into BTR suggests that investors view this segment as highly resilient. Its ability to offer stable, inflation-linked returns and its professionally managed model are particularly appealing to institutional investors seeking long-term stability in potentially volatile markets. The continued cross-border investment further reinforces the notion that global capital perceives the UK BTR market as a robust opportunity, potentially outperforming other real estate sectors or traditional asset classes during periods of economic uncertainty.

Role of Institutional Capital and Professionalization of the Private Rented Sector (PRS)

The UK BTR market has become a magnet for global capital, with cross-border investment increasing by 51% year-on-year in 2024, accounting for 66% of total investment. North American capital, in particular, has been a dominant force, reaching a record £2.8 billion and, for the first time, outstripping investment from the UK itself. Major institutional players, including Starlight, Legal & General (L&G), Lloyds Living, Sigma Capital, Leaf Living, Greykite, and Kennedy Wilson, are actively expanding their portfolios. L&G, for example, has deployed over £3 billion into the BTR sector since 2016, contributing to the delivery of more than 10,000 rental homes across the UK.

The growth of the BTR sector is fundamentally professionalizing the UK's Private Rented Sector (PRS), leading to an increasing market share for purpose-built rental properties. While BTR currently constitutes only 2% of the overall UK PRS, its footprint is significantly larger in major urban centers. In Manchester, for instance, nearly 25% of the PRS stock is now BTR. This expansion is also influenced by a trend of divestment from individual Buy-to-Let landlords, which contributes to the BTR sector's growth against a more stagnant traditional PRS.

The increasing market share of BTR in regional cities, particularly Manchester, suggests that these areas are leading the professionalization of the UK's rental sector. The high concentration of institutional-grade, purpose-built stock in Manchester indicates its role as a proving ground and a model for how BTR can integrate into and transform local housing markets. This implies that successful strategies and product innovations observed in Manchester are likely to be adopted in other developing regional BTR hubs, making Manchester a key indicator for the broader market's future direction and maturity.

Beyond multifamily developments, single-family housing (SFH) BTR is also cementing its position within the UK residential investment market. In 2024, investors allocated £1.8 billion to fund or acquire nearly 6,000 houses for rent, representing 36% of total BTR investment by value. Furthermore, 22% of the under-construction BTR pipeline is dedicated to houses for rent, indicating a diversification of product offerings within the sector. This expansion into SFH BTR points to an evolving understanding of renter demographics and preferences, acknowledging a demand for various housing types beyond central city apartments. This trend could unlock new investment avenues in suburban areas, catering to families or individuals seeking more spacious living environments.

Table 4: UK BTR Investment and Supply Overview (2024-2025)

Note: Data for Q1 2025 is partial and reflects available information for investment volumes and operational homes. Proportions for cross-border and SFH investment are primarily based on 2024 full-year data.

2. Manchester: A Prime BTR Investment Destination

Current Market Landscape: Operational Stock, Market Share in PRS

Manchester has firmly established itself as the largest BTR market in the UK outside of London. The city, including the adjacent boroughs of Salford and Trafford, currently boasts 34 operational BTR schemes, collectively providing 13,139 homes. This substantial operational stock accounts for 17% of the UK's total existing BTR units. The penetration of BTR within Manchester's Private Rented Sector (PRS) is particularly noteworthy, with nearly 25% of the PRS now comprising BTR properties. This figure significantly surpasses the national UK average of 2% for BTR's share of the PRS.

Economic and Demographic Drivers Fueling Rental Demand

Manchester's robust economic performance and favorable demographic trends are primary catalysts for its strong rental demand. The city's economy is projected to exhibit an average annual growth rate of 2.2% between 2024 and 2027, which comfortably outpaces the national growth rate of 2.1%. This positions Manchester as the second-fastest growing economy in the UK, only slightly behind Reading. The city's thriving tech, creative, and finance sectors contribute to a dynamic job market, attracting major corporate entities such as the BBC, ITV, Google, HSBC, and Microsoft.

Population growth in Manchester has been substantial, increasing from 422,000 to 600,000 inhabitants since the turn of the millennium, with an additional 30,000 residents anticipated within the next six years. The city centre alone is projected to accommodate 100,000 people by 2026. This demographic expansion is largely driven by a high graduate retention rate of 51.5% , drawing in young professionals, over 100,000 students from four major universities, and families who are attracted to the city's diverse job opportunities, vibrant cultural scene, and urban lifestyle. The high proportion of Manchester residents living in privately rented accommodation, estimated at 62%, further underscores the intense demand within the rental market.

The combination of surging population growth and a persistent imbalance between housing supply and demand creates a robust environment for continued rental price appreciation and high occupancy rates within Manchester's BTR sector. Despite significant new developments, the current supply is not keeping pace with the escalating demand, particularly from young professionals and students. This structural undersupply reinforces Manchester's attractiveness for BTR investors, as it helps ensure sustained rental income growth and capital appreciation. The strategic decision by developers to significantly increase BTR unit counts in projects like Albert Bridge House, doubling them to approximately 800 units, is a direct market response to this acute and unmet demand.

Detailed Property Market Performance (May 2025 data)

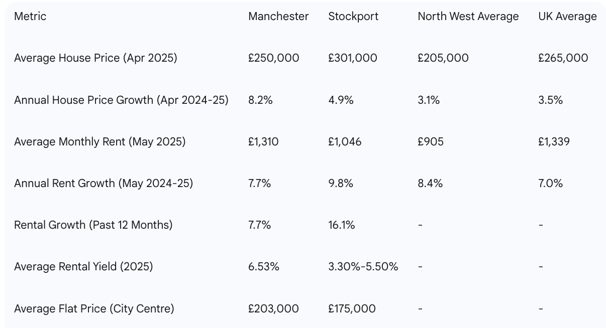

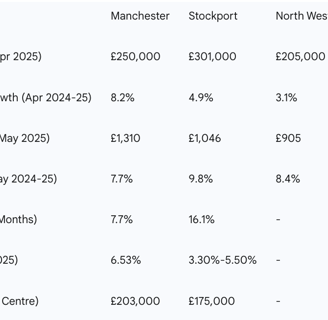

As of April 2025, the average house price in Manchester stood at £250,000, representing an 8.2% increase from April 2024. This growth rate was notably higher than the North West regional average of 3.1% over the same period. The average monthly private rent in Manchester reached £1,310 in May 2025, reflecting an annual increase of 7.7% from May 2024, though this was slightly below the North West average of 8.4%.

Within Manchester's diverse property types, flats and maisonettes experienced an 8.5% increase in purchase prices and an 8.0% rise in rental values. The average rental yield in Manchester in 2025 was 6.53%, which is higher than London's 4.95%, indicating strong income potential for investors. Specific average monthly rents by bedroom count in May 2025 were: £959 for one-bedroom properties, £1,180 for two-bedrooms, £1,364 for three-bedrooms, and £1,946 for four or more bedrooms.

Overview of Key BTR Developments: Completed, Under Construction, and Planned Projects

Manchester's BTR landscape is dynamic, with a substantial pipeline of developments. The city's pipeline of 16,975 BTR units is the third largest among UK cities, trailing only London and Birmingham.

Operational Schemes: Notable operational schemes include Downing Living's Square Gardens, which, with 1,319 co-living units, is the largest co-living development in the UK. Other prominent operational BTR schemes include Moda Living's Angel Gardens (466 units) and Dandara Living's Chapel Wharf (995 units). Allsop manages the highest number of operational BTR schemes in Manchester, while Grainger is the second-largest operator with 1,125 units across three schemes. Legal & General's "The Slate Yard" is another key operational development.

Under Construction and Planned Projects: Recent planning approvals include 364 BTR units at Whitworth Street West (April 2025), 237 units at Cheetham Hill Road, and 359 units at Sparkle Street (both November 2024). In March 2025, CERT submitted plans for 104 units at Cross Keys Street, and Landsec submitted plans for 879 units at Mayfield Park.

Major ongoing or planned projects include:

Albert Bridge House: Revised plans submitted in June 2025 propose to double the number of BTR homes to approximately 800 across two towers (49 and 37 storeys), with a reduction in commercial space.

One Port Street, Northern Quarter: A £130 million BTR development offering 477 premium apartments with luxury amenities.

Deansgate Square, New Jackson Neighbourhood: Features four iconic towers housing 1,508 luxury apartments with extensive amenities. Legal & General's partnership with Nest and PGGM recently acquired the F1 site in New Jackson, planning 494 purpose-built apartments.

Piccadilly East: A £75 million BTR scheme that will deliver 196 apartments across two buildings.

Property Alliance Group's AXIS: A 28-storey landmark residential tower with 170 luxury apartments.

Uptown Manchester: A trio of residential towers along the River Irwell, delivering 156 BTR apartments with a focus on sustainable features.

Manchester Waters, Trafford: Recently approved for the construction of 159 BTR apartments across two buildings on a brownfield dockland site.

Victoria North: This significant urban regeneration project in North Manchester is set to add another 15,000 new homes.

Table 2: Major BTR Developments in Manchester (Operational, Under Construction, Planned)

Note: This table provides a snapshot of major developments. "Status" reflects the most recent information available. "Number of Units" may vary slightly based on final designs.

Analysis of Major Developers and Institutional Investors Active in Manchester

The Manchester BTR market is significantly shaped by the involvement of major developers and institutional investors. Key developers include Legal & General, known for its "The Residences" and "The Slate Yard" schemes, and its recent acquisition of the F1 site in New Jackson for 494 purpose-built apartments through a partnership with Nest and PGGM. Rise Homes, an award-winning developer specializing in sustainable development, also has a presence with "Route 1 @ The Depot" and "The Depot" in Manchester. While Plumlife's "Platform, Stockport" is primarily Stockport-focused, its regional activity signals broader engagement in Greater Manchester.

Institutional investment in Manchester's BTR sector has been substantial, with £148.6 million invested in BTR schemes in 2023 alone, demonstrating strong market confidence and demand. Maven Capital Partners maintains a long-term presence in Manchester, operating one of the largest investment teams in the North West. While their investments span various growth industries, their focus on ambitious businesses in the region suggests potential for broader property investment, including BTR. The continued influx of capital from both domestic and international institutional players underscores Manchester's appeal as a leading destination for BTR investment.

3. Stockport: An Emerging BTR Investment Hub

Market Overview: Strategic Location, Commuter Appeal, and Regeneration Impact

Stockport is strategically positioned within Greater Manchester, making it a pivotal commuter town for Manchester. Over 12% of Manchester residents have chosen to relocate to Stockport, highlighting its growing appeal as an attractive alternative for renters. Its proximity to affluent Manchester suburbs further enhances its desirability.

The town is currently undergoing a transformative £1 billion regeneration program, one of the largest in the UK, which has already significantly reshaped its Town Centre West area. This overhaul includes a new transport interchange, additional housing provisions, and the creation of new commercial and social spaces, all of which are attracting businesses and residents and elevating Stockport's status. The Stockport Mayoral Development Corporation is a key driver in this transformation, with plans to deliver 8,000 new homes. Looking ahead, the Strategic Regeneration Framework for Stockport Town Centre East aims to guide urban regeneration until 2040, targeting the delivery of an additional 4,000 high-quality homes, new social and physical infrastructure such as a health hub, a secondary school, and an urban park in Piccadilly, alongside new employment opportunities.

The exceptionally high rental growth in Stockport, combined with its ongoing regeneration efforts and relative affordability compared to Manchester, suggests a significant "catch-up" dynamic in the market. As Manchester's rental market matures and becomes more expensive, demand is naturally spilling over into well-connected, regenerating commuter towns like Stockport. This market dynamic implies that Stockport offers higher immediate growth potential for rental income, making it a compelling target for investors seeking robust yields and capital appreciation driven by rapid market revaluation rather than just steady growth. The regeneration initiatives are actively accelerating this revaluation by enhancing amenities and connectivity, further amplifying the town's attractiveness.

Property Market Performance (May 2025 data)

Stockport's property market has demonstrated strong performance. The average house price in Stockport was £301,000 in April 2025, marking a 4.9% increase from April 2024. This growth rate surpassed the North West average of 3.1% and positioned Stockport with the third-highest average house price in the region.

In the rental sector, the average monthly private rent in Stockport reached £1,046 in May 2025, representing an impressive annual increase of 9.8% from May 2024. This was higher than the North West average of 8.4%. Notably, Stockport experienced the second-fastest rental growth across the UK, with a significant 16.1% surge in rents over the past 12 months. Average rental yields in Stockport range from 3.30% to 5.50%, with the town centre (SK1) and Reddish (SK5) leading with yields of 5.50%.

Property prices in Stockport offer strong value compared to UK averages, particularly for detached and semi-detached housing, where prices exceed the national average by 15% and 13% respectively. Flats and maisonettes, however, provide more accessible entry points, with prices 24% below national averages. Average rents by bedroom count in May 2025 were: £757 for one-bedroom properties, £965 for two-bedrooms, £1,182 for three-bedrooms, and £1,652 for four or more bedrooms.

Demographic Shifts and Their Influence on Rental Demand

Demographic shifts in Stockport are significantly influencing rental demand. The proportion of households privately renting has increased substantially, rising from 11.4% in 2011 to 14.4% currently. Concurrently, home ownership has seen a slight decrease from 73.2% to 71.1%.

Age-related population changes between 2011 and 2021 further illuminate the evolving demand landscape. The number of residents aged 65-74 years increased by over 4,400 people (a 16.7% rise), while the 35-49 age group experienced a reduction of approximately 3,100 people (a 4.9% decrease). These demographic changes indicate that rental demand in Stockport is not solely driven by the traditional cohort of young professionals typically associated with city-centre BTR. The observed increase in older renters and the overall rise in private renting across the population, coupled with the strong performance of larger property types, suggest a broader appeal for BTR. This implies that investors in Stockport have opportunities to diversify their BTR portfolios beyond typical city-centre apartments, potentially exploring purpose-built housing for families or senior living. Such diversification would align with the observed demographic shifts and cater to a wider range of rental preferences, offering a broader spectrum of investment products.

Key BTR Developments: Planned and Existing Projects

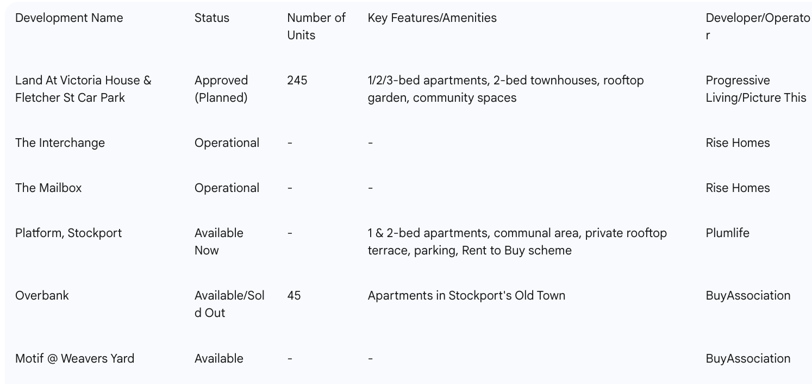

Stockport's BTR market, while emerging, is seeing significant planned development.

Planned Developments: The most prominent planned BTR scheme is the Land At Victoria House and Fletcher Street Car Park project. This £70 million development has received approval for 245 homes, comprising 100 one-bedroom, 91 two-bedroom, and 42 three-bedroom apartments, along with 12 two-bedroom townhouses. Demolition work is anticipated to commence in 2025, with construction slated to begin in spring 2026, following BSA Gateway 2 approval. The target completion date for this project is summer 2028. This BTR development is a collaborative effort between Progressive Living and Picture This, benefiting from financial support from the Greater Manchester Combined Authority brownfield fund.

Existing/Available Projects: Rise Homes has a presence in Stockport with "The Interchange" and "The Mailbox" developments. Plumlife offers "Platform, Stockport" apartments, which are available through a Rent to Buy scheme and feature communal areas, private rooftop terraces, and allocated parking spaces. Additionally, BuyAssociation lists "Overbank" (45 apartments) and "Motif @ Weavers Yard" as current and upcoming investment opportunities in Stockport.

Table 3: Major BTR Developments in Stockport (Operational, Under Construction, Planned)

Note: "Number of Units" may not be available for all operational/available schemes in the provided data. Status reflects the most recent information available.

Local Investment Landscape and Unique Opportunities

Stockport's property market has demonstrated robust value, having quickly recovered from a brief dip in 2021-2022 and continuing on a growth trajectory. The town centre (SK1) has shown exceptional performance, recording a 42% 5-year growth, outperforming other areas like Heaton Moor (SK4) at 32.2%.

The local investment landscape is supported by entities such as HG Financial Planning, an independent financial advisor based in Stockport, offering investment advice to local clients. BuyAssociation actively promotes Stockport as a prime target for property investors, citing the strong existing demand and the significant future improvements stemming from the £1 billion regeneration program as factors that will yield excellent returns through both rental income and capital appreciation. For investors considering Houses in Multiple Occupation (HMOs), Stockport's licensing fees, as of February 2025, are £1,115 for new licenses (up to 5 bedrooms) and £950 for renewals, with additional fees for extra rooms. This regulatory detail is important for specific investment strategies within the rental market.

4. Comparative Investment Analysis: Manchester vs. Stockport

Direct Comparison of Market Metrics (May 2025 data)

A direct comparison of key property market metrics reveals distinct profiles for Manchester and Stockport, offering different strategic advantages for BTR investors.

Table 1: Key Property Market Metrics (Manchester vs. Stockport, May 2025)

Note: Some data points are specific to city/town centres or broader areas as per source. "Past 12 Months" rental growth for Stockport is from Rightmove data, while "Annual Rent Growth" for May 2025 is ONS data.

Analysis of Demand Drivers, Supply Dynamics, and Investment Attractiveness in Each Location

Manchester: Manchester's BTR market is driven by a robust economy, significant population growth, and a high graduate retention rate, positioning it as a mature BTR hub with a large operational stock and a substantial development pipeline. Demand is exceptionally strong, particularly from young professionals and students, leading to high occupancy rates and attractive rental yields. The market is characterized by larger, high-density multifamily developments, reflecting its urban core status.

Stockport: Stockport's market is propelled by extensive urban regeneration, increasing commuter appeal due to its relative affordability compared to Manchester, and evolving demographics. It has experienced rapid rental growth and offers more accessible entry points, especially for flats. The market is less saturated with BTR developments but is quickly emerging as a viable alternative for investors seeking value and high growth potential.

The comparison of average house prices and rents between Stockport and Manchester highlights a critical "affordability arbitrage" that is driving rental migration and creating distinct investment opportunities. Average rents in Stockport (£1,046) are considerably lower than in Manchester (£1,310). Similarly, the average price of a flat in Stockport town centre (£175,000) is more affordable than in Manchester city centre (£203,000). This price differential is a key factor in Stockport being identified as the "number one Manchester commuter town," with over 12% of Manchester dwellers choosing to relocate there. Furthermore, only 36% of tenants moving house in Manchester last year remained within the city. This outward migration, driven by the rising cost of living in Manchester, directly fuels demand in Stockport, contributing to its remarkable rental growth rate of 16.1% compared to Manchester's 7.7%. For BTR investors, this dynamic presents a strategic opportunity to capitalize on this tenant movement by developing or acquiring properties in Stockport. This allows them to offer a more attractive price point for tenants while still benefiting from the proximity to Manchester's robust job market, potentially leading to higher yields for new investments in an emerging market.

A deeper examination of the property valuation metrics reveals a nuanced difference in market composition. Stockport's average house price (£301,000) is higher than Manchester's (£250,000) , even though Stockport's average monthly rent (£1,046) is lower than Manchester's (£1,310). This apparent contradiction can be attributed to the differing housing stock. Manchester has a higher proportion of flats and apartments (28%) compared to Stockport (15%), and areas with a greater concentration of flats generally exhibit lower average house prices. Conversely, Stockport's property market demonstrates strong value in detached and semi-detached properties, which often command higher prices. For BTR investors, this implies that Manchester offers opportunities for high-density, typically smaller-unit BTR developments that can achieve higher per-unit rents. In contrast, Stockport's market, despite lower average rents, may present opportunities for single-family BTR or larger apartment units, potentially with different yield profiles. This necessitates a sophisticated investment strategy that recognizes these underlying compositional differences and tailors development or acquisition approaches accordingly.

Strategic Advantages and Considerations for Investors in Both Cities

Manchester: Offers stability, a proven track record of BTR success, high rental yields, and a deep pool of institutional-grade assets. It is ideal for investors seeking large-scale, professionally managed multifamily developments within a dynamic urban core. However, competition for prime assets remains high, and property prices are generally higher than in Stockport for comparable property types.

Stockport: Presents a compelling growth narrative with exceptional rental growth rates and significant capital appreciation potential, largely due to ongoing regeneration efforts. It offers more accessible entry points for certain property types and could appeal to investors seeking higher immediate rental growth and value-add opportunities. Its role as a commuter hub suggests sustained demand from tenants who are priced out of Manchester's city core.

A strategic approach could involve diversifying portfolios across both locations. This balanced strategy would allow investors to leverage Manchester's established performance and scale while capitalizing on Stockport's high-growth potential and emerging market dynamics.

5. Challenges, Risks, and Regulatory Environment

Identification of National Challenges

The UK BTR sector, despite its robust growth, faces several significant national challenges:

Supply Shortfall: The UK continues to grapple with a profound housing crisis, characterized by an acute shortage of homes. Despite record BTR completions, demand persistently outpaces supply, contributing to ongoing housing pressures.

High Capital and Construction Costs: Escalating construction costs, driven by inflationary pressures, labor shortages, and supply chain disruptions, have rendered many development schemes financially unviable without public or private subsidies. Managing operational costs while delivering high-quality services remains a continuous challenge for BTR operators.

Planning System Inefficiencies: Persistent delays within the planning process and, in some instances, skepticism from local authorities, hinder project viability and slow down development programs. Streamlining approval systems is crucial for accelerating delivery.

Regulatory Changes: The evolving regulatory landscape significantly impacts project viability. The Building Safety Act, in particular, has introduced additional delays and costs, especially for high-rise developments. BTR operators must navigate a complex array of rental regulations, including deposit protection, right to rent checks, and health and safety requirements, with non-compliance carrying risks of fines and reputational damage.

Taxation Changes: Recent changes, such as the abolition of multiple dwellings relief for Stamp Duty Land Tax and increased surcharges for non-UK residents, have negatively affected investment appraisals, particularly in regions outside London and the South East.

Political Instability: Periods of political volatility, including the aftermath of Brexit and abrupt policy shifts, have at times deterred both domestic and international investors.

The regulatory environment, particularly the Building Safety Act, presents a complex challenge for BTR supply. While the Act aims to enhance safety, it has introduced additional delays and costs, especially for high-rise developments. This is particularly pertinent for Manchester, where the BTR market is heavily reliant on high-rise, multifamily developments, with a significant pipeline of such projects. This regulatory friction exacerbates the existing supply shortfall, potentially slowing down the delivery of much-needed homes and exerting further upward pressure on rents in the short to medium term. For investors, this translates to longer development timelines and increased costs, necessitating meticulous financial modeling and risk assessment for new high-rise BTR projects. Conversely, it could also reinforce the value and appeal of existing, stabilized BTR assets that have already navigated these hurdles.

Local Challenges Specific to Manchester and Stockport

Beyond national headwinds, specific local challenges exist:

Stockport HMO Licensing Fees: For Houses in Multiple Occupation (HMOs), new licenses (up to 5 bedrooms) cost £1,115, and renewals are £950, with additional fees for more rooms (as of February 2025). These fees contribute to the operational costs for specific types of rental properties in Stockport.

Building Safety Delays: The broader implications of the Building Safety Act could disproportionately affect high-rise BTR developments prevalent in Manchester, potentially delaying project completions and impacting investment returns.

Affordability Concerns: While rising rents drive demand, they also pose affordability challenges for tenants. Nationally, rents have increased by 40% since 2020, compared to a 31% increase in wages. If not managed with innovative solutions, this growing affordability gap could eventually impact tenant retention and lead to higher void periods.

Strategies for Mitigating Risks and Ensuring Long-Term Viability

To navigate these challenges and ensure long-term viability, several strategic approaches are recommended:

Policy Reform and Industry Collaboration: Advocating for systemic policy reforms, such as a dedicated planning use class for BTR and improved coordination between housing and infrastructure planning, is essential to unlock further growth.

Cost Management: Developers must continuously balance quality and affordability through innovative building techniques, economies of scale, and strategic partnerships to optimize project viability.

Proactive Tenant Management: Implementing loyalty programs, offering incentives for lease renewals, and fostering community engagement through social events can significantly boost tenant retention. Utilizing predictive analytics within management software can help identify tenants at risk of leaving, allowing for proactive intervention.

Technology Adoption: Leveraging technology for operational efficiency, such as automated maintenance requests, streamlined rent collection, and digital record-keeping for compliance, can reduce manual workload and minimize human error.

Stakeholder Management: Effective communication and collaboration tools are vital for coordinating the diverse interests of property owners, investors, tenants, and service providers, ensuring smooth operations.

Sustainable Development: Incorporating green building practices, energy-efficient systems, and smart technology into BTR projects aligns with broader sustainability goals and future-proofs assets, enhancing their long-term appeal and value.

The evolving role of BTR in addressing broader housing and social objectives is becoming increasingly significant. BTR is recognized as a strategic opportunity for both investors and policymakers, playing a meaningful role in urban regeneration, housing provision, and wider social objectives. It is also considered a crucial component of local authorities' housing strategies. There is a growing emphasis on diversifying product offerings within the BTR sector to include affordable housing options. Greater Manchester's overarching housing plan, for instance, aims to increase the provision of affordable, social, and net-zero housing, with brownfield fund grants actively supporting affordable housing initiatives. This indicates a shift beyond BTR purely as a commercial investment vehicle towards a more integrated role in public policy and urban planning. As the BTR sector matures, its success will increasingly depend on its ability to align with local authority housing strategies, contribute to urban regeneration, and address social objectives like affordability and sustainability. This implies that future BTR projects, particularly in areas like Stockport undergoing significant regeneration, may need to incorporate elements of affordable housing, green building practices, and robust community integration to secure planning approvals and public support, thereby influencing investment criteria and project design.

6. Future Outlook and Strategic Recommendations

Expert Forecasts for BTR Market Evolution in Manchester and Stockport

The Build-to-Rent sector in both Manchester and Stockport is poised for continued robust growth, underpinned by strong investor appetite, favorable economic outlooks, and persistent demand for rental properties.

Manchester Forecasts: Manchester is projected to remain a leading regional market. JLL forecasts Manchester to be the second strongest UK city for house price growth until 2028, with prices anticipated to increase by 19.3%, surpassing the national growth projection of 17.6%. Rental values are expected to see an average annual increase of 4% until 2028. City centre rents are specifically projected to continue their upward trajectory, potentially reaching £47 per square foot by 2027. The city's ongoing population growth, particularly within the city centre, is expected to ensure sustained rental demand.

Stockport Forecasts: Stockport is anticipated to sustain its impressive rental growth trajectory, building on its recent 16.1% surge. This growth will be driven by its ongoing regeneration efforts and its increasing role as an attractive, more affordable commuter alternative to Manchester. The substantial £1 billion regeneration program and planned future infrastructure improvements are expected to deliver excellent returns through both rental income and capital appreciation.

Overall Market Dynamics: Despite increasing delivery of new BTR units, the fundamental supply-demand imbalance is expected to persist in both locations, maintaining upward pressure on rental rates. There is a growing emphasis across the sector on innovation and sustainability, with developers increasingly incorporating green building practices and smart technology into their projects, aligning with broader environmental goals. Furthermore, the BTR sector is expected to continue diversifying its product offerings to meet a wider range of tenant needs, including co-living spaces, senior living communities, and affordable housing options.

The explicit focus on sustainability within the development plans for both Manchester and Stockport, coupled with developers actively adopting green practices, indicates that Environmental, Social, and Governance (ESG) considerations are no longer merely beneficial but are becoming critical drivers for BTR investment. This suggests that future BTR projects that integrate robust sustainability features are likely to benefit from more streamlined planning approvals, attract a growing segment of environmentally conscious tenants, potentially command premium rents, and appeal to institutional investors with strong ESG mandates. Conversely, projects that neglect these aspects may face regulatory hurdles, reduced tenant appeal, and limited access to capital, making ESG integration an imperative for long-term viability and competitive advantage in these markets.

The emphasis on communal amenities, on-site services, and broader urban regeneration efforts points to "placemaking" as a crucial strategy for BTR success. It extends beyond merely providing housing units to creating a desirable lifestyle and a vibrant community. This implies that BTR investments prioritizing well-designed communal spaces, fostering a sense of belonging among residents, and integrating seamlessly with the surrounding neighborhood—through public realm improvements, and access to jobs and services—are likely to achieve higher tenant satisfaction, lower void periods, and stronger brand loyalty. This differentiation is vital in an increasingly competitive rental market and directly contributes to the long-term profitability and attractiveness of the BTR asset.

Actionable Recommendations for Continued Investment

Based on the comprehensive analysis, the following actionable recommendations are provided for continued investment in purpose-built rental properties in Manchester and Stockport:

Strategic Allocation: Investors should adopt a balanced portfolio approach. This involves leveraging Manchester's established market and strong yields for stable, large-scale investments, while simultaneously capitalizing on Stockport's high-growth potential and value-add opportunities in its emerging market.

Focus on Regeneration Zones: Prioritize investments in areas undergoing significant urban regeneration, such as Stockport Town Centre West/East and Manchester's Victoria North. These zones benefit from enhanced infrastructure, improved amenities, and sustained demand driven by renewed vitality.

Diversify Product Types: Explore opportunities beyond traditional multifamily apartments. Consider single-family BTR (SFH) in Stockport and other Greater Manchester suburbs to cater to evolving demographic needs and preferences, including families and older renters.

Embrace Sustainability and Technology: Integrate eco-friendly designs, energy-efficient systems, and smart home technology into all new developments. This approach attracts modern tenants, contributes to reduced operational costs, and aligns with increasingly important environmental, social, and governance (ESG) investment criteria.

Navigate Regulatory Landscape: Engage proactively with local planning authorities and remain informed about evolving regulatory changes, particularly concerning building safety and rental legislation. This proactive stance helps mitigate risks and ensures project viability. For specific strategies, the implications of HMO licensing in Stockport should be carefully considered.

Leverage Local Expertise: Partner with experienced local developers, property managers, and financial advisors. Their deep market knowledge and understanding of regional nuances are invaluable for identifying optimal opportunities and navigating specific local challenges.

Community-Centric Development: Focus on creating vibrant communities within BTR developments. This includes providing generous communal facilities, organizing social activities, and ensuring responsive on-site management. Such an approach enhances tenant satisfaction, fosters a sense of belonging, and contributes significantly to tenant retention and brand loyalty.